In 2021, loss-making entities and cryptos were all the rage.

No price was too high to pay…at least, that’s what the gullible and greedy thought.

In 2022, people are starting to pay a very high price to learn the difference between falsehoods and facts.

Four Corners and 60 Minutes are belatedly reporting on the perils of the crypto con.

In the US, the Commodity Futures Trading Commission (CFTC) is (also, belatedly) flexing its muscles.

Legal action has been commenced against the Winklevoss twins (the ones who claimed Mark Zuckerberg stole their idea for Facebook).

I reckon Zuckerberg might have cracked a wry smile when this news broke (emphasis added):

‘The Winklevoss twins’ Gemini Trust Co. is being sued by the Commodity Futures Trading Commission for allegedly misleading the derivatives regulator in a bid to launch the first US-regulated Bitcoin futures contract.

‘The CFTC said Thursday that Gemini “made false and misleading statements” from July to December 2017 about how it would prevent manipulation in Bitcoin prices that were to serve as a reference for the derivatives based on the cryptocurrency.

‘In a lawsuit filed in federal court in Manhattan, the agency sought trading and registration bans, as well as fines.’

Bloomberg, 3 June 2022

Shock, horror!

Claims of ‘false and misleading statements’ concerning Bitcoin [BTC]…geez who woulda thunk that?

Naturally, the twins are denying any such falsehoods were made.

Now it’s over to the legal system to decide whose is the truer version of the truth.

On the topic of wry smiles…last week, I received this chart on how far (a selection of) the mighty have fallen.

The reason for circling five stocks will become apparent shortly:

|

|

|

Source: YCharts |

With the S&P 500 Index only down 17% from its high, the bear has not yet GROWLED loud enough for the financial press to declare ‘It’s a BEAR…run for your life!’.

As evidenced by the above chart, this bear is stalking its prey in stealth mode…selectively maiming and mauling individual stocks.

Widespread carnage WILL follow.

How can I be so sure?

Let me take you back to an article I wrote in The Rum Rebellion on 4 May 2021 titled:

‘Belief in the Holy Grail Leads to One Hell of a Fail’.

Here’s an edited extract:

‘I get it…it’s different this time.

‘This market is an entirely different beast…neither bull nor bear.‘In its quest to bound from one peak to another, it occasionally pauses for breath.

‘Sometimes losing its footing…but springs back swiftly to recover lost ground.

‘We have been blessed with the Holy Grail of markets…one with unlimited upside and only minimal downside.

‘To experience this in your lifetime…can you believe your good fortune?

‘I thought I caught a glimpse of this phenomena in 1987…but alas, it was a fake.

‘In 2000, oh, how we thought the new paradigm was the real deal…only to be left disappointed.

‘The years leading up to 2008…this was definitely it.

‘Uninterrupted exponential growth was ours for the taking.

‘Borrow to invest and ride the wave of never-ending prosperity to a wealth beyond your wildest dreams.

‘Well, that kind of happened. People with margin debt never, in their wildest dreams, thought they could lose all their money.

‘Don’t dwell on the past. That was then, not now.

‘If you weren’t there in the late 1990s, here’s a reminder (courtesy of Wikipedia) of what it was like in the heady days of the late 1990s (emphasis added):

“At the height of the boom, it was possible for a promising dot-com company to become a public company via an IPO and raise a substantial amount of money even if it had never made a profit—or, in some cases, realized any material revenue.

“Most dot-com companies incurred net operating losses as they spent heavily on advertising and promotions to harness network effects to build market share or mind share as fast as possible, using the mottos ‘get big fast’ and ‘get large or get lost’.”

‘Sound vaguely familiar?

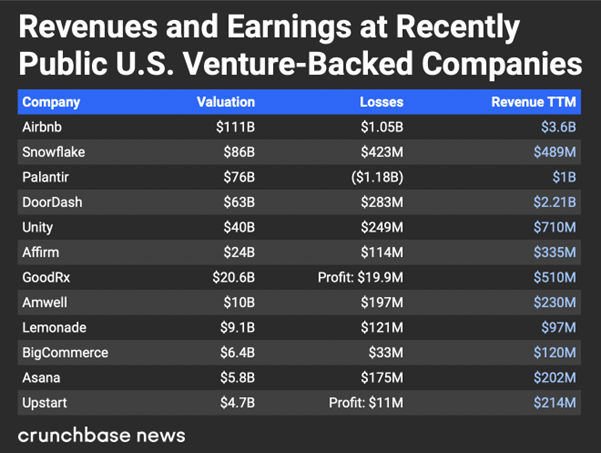

‘Here’s what Crunchbase News found when it ran the ruler over 12 venture capital-backed companies that went public in the second half of 2020:

|

|

|

Source: Crunchbase News |

‘With the Fed underwriting debt issues, why would anyone think history is repeating itself?

‘Those dotcom negatives were real negatives that could not be sustained. They deserved to be punished in a near 80% fall on the Nasdaq.

‘But today’s negatives are entirely different. Profits are so yesterday. Scale and growth are what matter.

‘As reported by CNBC on 9 February 2021:

“For all of 2020, Uber’s net losses amounted to $6.77 billion, around a 20% improvement from a staggering $8.51 billion loss in 2019.”

‘And what do investors get for being part of an entity that tore up US$6.77 billion in 2020?

‘Uber is currently valued at US$104 billion.’

My tongue-firmly-planted-in-cheek article included five of the companies — Snowflake, Palantir, DoorDash, Unity, and Uber — in the YCharts’ ‘name-and-shame’ table.

Here’s how the others have fared:

| Company | Valuation May 2021 | Valuation June 2022 | % change in valuation |

| Airbnb | US$111 billion | US$76 billion | MINUS 32% |

| Affirm | US$24 billion | US$7 billion | MINUS 71% |

| GoodRx | US$20.6 billion | US$3 billion | MINUS 85% |

| Amwell | US$10 billion | US$1 billion | MINUS 90% |

| Lemonade | US$9.1 billion | US$1.3 billion | MINUS 86% |

| BigCommerce | US$6.4 billion | US$1.3 billion | MINUS 80% |

| Asana | US$5.8 billion | US$4.3 billion | MINUS 26% |

| Upstart | US$4.7 billion | US$4.1billion | MINUS 13% |

Underneath the surface of the broader S&P 500 Index, there’s real damage being done to portfolios with an overweighting in yesterday’s high-flyers.

Those invested in an S&P 500 Index fund (and even the ASX 200) are not feeling the same pain…YET!!!

The bear ALWAYS snacks on the most vulnerable (the excessively overpriced) first. This is merely the entrée course.

With its once-dormant metabolism awakened, the ravenous bear goes in search of its main course…the broader market.

To quote from The Rum Rebellion article (emphasis added):

‘My disbelief in this whole “it’s different this time” thing stems from being old-school.

‘Normally, when a company publicly states there’s a “snowball’s chance in hell” of ever being profitable, the logical conclusion would be the company is worthless.

‘However, there have been times in market history when logic is suspended. A fleeting period when the worthless is mistakenly viewed as a highly prized asset.

‘Anyway, back to the boring stuff…market history.

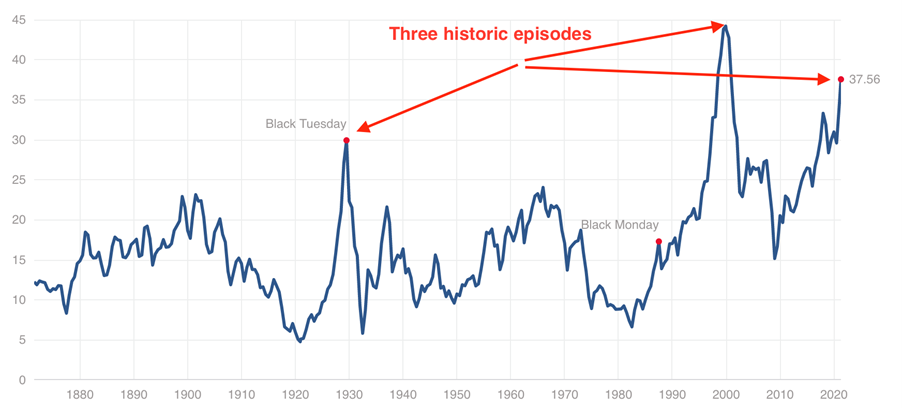

‘We know the more famous episodes of investors being duped by the “it’s different this time” myth were in 1929 and 2000…and, call it a hunch, but possibly this time as well:

|

|

|

Source: Multpl.com |

‘We know the dotcom bubble incubated its fair share of loss-making entities, but what about 1929?

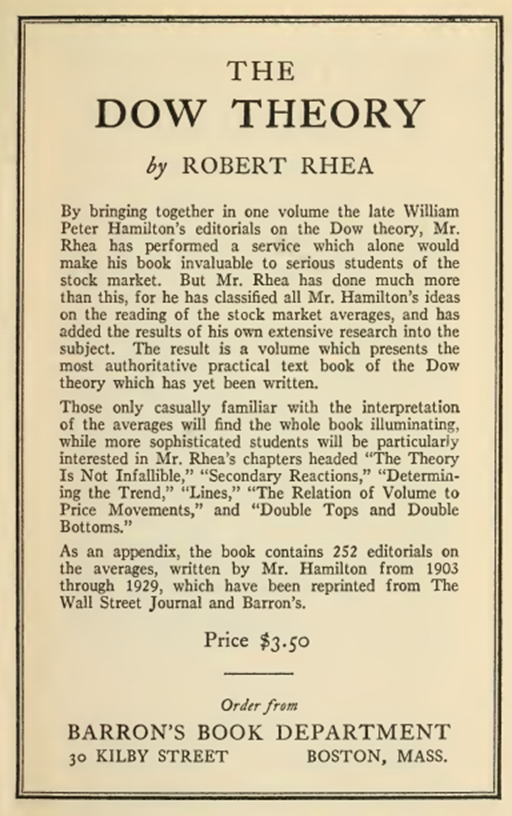

‘In 1932, Robert Rhea authored the The Dow theory.

‘The introduction tells you all you need to know…this was a serious book about a serious topic for serious readers:

|

|

|

Source: University of Toronto |

‘According to Investopedia…

“The Dow Theory is an approach to trading developed by Charles H Dow who, with Edward Jones and Charles Bergstresser, founded Dow Jones & Company, Inc and developed the Dow Jones Industrial Average (DJIA). Dow fleshed out the theory in a series of editorials in the Wall Street Journal, which he co-founded.”

‘In a nutshell, the Dow theory is an old-school approach to value investing.

‘The boring, logical stuff that keeps you grounded while others indulge in their ill-fated flights of fantasy.

‘In his 1932 book, Robert Rhea wrote about the period leading up to the 1929 crash (emphasis is mine):

“Worthless equities were being sky-rocketed without regard for intrinsic worth or earning power. The whole country appeared insane on the subject of stock speculation. Veteran traders look back at those months and wonder how they could have become so inoculated with the ‘new era’ views as to have been caught in the inevitable crash. Bankers whose good sense might have saved the situation, had speculators listened to them, were shouted down as deconstructionists, while other bankers, whose names will go down in history as ‘racketeers’, were praised as supermen.”

‘Well, what do you know…people were speculating in worthless companies back in the late 1920s.

‘Today’s obscene values being afforded to loss-making enterprises is nothing more than a repeat of previous periods of excess.

‘There is nothing different about this. It’s just man doing what man does…getting swept up in a rising tide of emotion.

‘Books like The Dow Theory are tiresome, unexciting, and dreary. People want razzle-dazzle, not dull and dismal.

‘There is nothing new about this.

‘Every generation of investors wants to believe they are special…they are different. But they’re not.

‘They fall for the same confidence tricks as their fathers and forefathers.

‘Is it just sheer coincidence the late 1920s, late 1990s, and the present register the three highest readings on multiples paid for (the average of the past 10 years of) earnings?

‘I think not.

‘However, in the current market, I accept mine is a minority opinion.‘Faith in the Holy Grail of “unlimited upside with minimal downside” is almost absolute.

‘No one can see how, why, or when this market goes from being the Holy Grail to one hell of a fail.

‘But, like all previous periods of belief in the market’s invincibility, it too will end in disbelief.’

At this early stage of the everything bubble deflating, the degree of disbelief depends upon how much skin individual investors have lost.

If you’ve only been scratched, you might still believe in the ‘this-time-is-different’ myth.

Give it time…the bear is coming for all those who fail to heed the same warnings our fathers and forefathers also ignored.

By the time the headlines report the GROWL, it’ll be yet another case of ‘too little, too late’.

When the bear finishes feasting, the broader US indices may finish down more than 60% in value…don’t expect the ASX to be spared from the worst of this.

Regards,

|

Vern Gowdie,

Editor, The Daily Reckoning Australia